At its core, a syndication is simply a collaboration—a partnership between two groups of people, each looking to generate financial gains through the purchase and ownership of an expensive asset that neither group (and none of the individuals in either group) would likely have the means to purchase on their own.

General Partner and Limited Partners

These two groups are known as the general partners (sometimes referred to as the GPs) and the limited partners (sometimes referred to as the LPs). The GPs and LPs are fundamental to the structure of any syndication, each playing a distinct role that is critical to the success of the investment.

General partners (GPs)

The general partners operate the syndication (hence why they are often referred to as “operators”). They are responsible for nearly all aspects of the investment—identifying the specific asset, negotiating the purchase, ensuring that the capital is available to complete the project, operation of the asset after purchase and then ultimately, sale of the asset.

Additionally, GPs are the decision makers. They have the final say over what asset(s) are purchased, how they are managed, and when they are sold. They are responsible for putting together the investment strategy and business plan, ensuring that everything runs smoothly from start to finish.

Because of their active role, GPs usually have significant investment experience, and a well-rounded GP team will have all the skills necessary to navigate complex transactions—legally, operationally, and financially.

Based on this, you may be wondering why the GPs need the partnership with another group of people. While the GPs have all the skills and experience to manage a deal from start to finish, the one thing they generally don’t have is all the capital to do so. That’s where the LPs come in.

Limited partners (LPs)

On the other side of the partnership are the limited partners, who contribute capital to the deal, generally in a hands-off—or passive—manner (hence why they are often referred to as “passive investors”). LPs are not involved in the decisions around which asset(s) to purchase, don’t get involved in day-to-day management of the property, and don’t have much—if any—say into when an asset is sold, to whom, or for how much.

LPs are looking for a way to invest without the hassles of having to operate the investment. By partnering with operators and pooling their money with other passive investors, they can take part in larger, more lucrative deals that would be out of reach as an individual investor.

Except in very limited circumstances, LPs have essentially no decision-making authority in the investment once they have committed their funds. They are putting their trust in the GPs to make optimal investment decisions that will generate returns on their investment over the next several years.

Neither the general partners nor the limited partners could complete an investment without the other. The general partners bring their time, effort, and skills, relying on the limited partners’ capital. The limited partners bring the capital, relying on the general partners to provide the expertise. Together, they can do larger—and more profitable—investments than either could do on their own.

When the syndication is structured properly, the LPs should have no legal exposure, and the extent of their risk is their investment in the deal. In fact, this is where the “limited” in “limited partner” comes from—the partner has limited liability and exposure, not extending past their financial investment.

The Syndication Structure

We’ve been talking about syndications generally, as a way to purchase large investment assets. And while we are focused on real estate, it’s important to note that syndications can be used to purchase any asset.

When venture capitalists or smaller angel investors invest in the next Google or Tesla, they generally do it using this same syndication structure. Expensive artwork can be purchased through a syndication structure. Even sports franchises are often purchased using this structure, with an ownership group (the general partners) buying a sports team using the capital of other investors who want to be part owners (the limited partners).

Real estate syndications

But again, we’re talking about real estate assets. And because syndications are typically reserved for larger, more expensive assets, in the real estate world, we often see syndications used to purchase more expensive commercial properties. Everything from apartment complexes to self-storage facilities to ground-up subdivision construction is commonplace in real estate syndication.

GPs in real estate syndications are likely to be long-time real estate investors looking to purchase larger properties than they can afford on their own. LPs in real estate syndications are looking to benefit from real estate ownership without having to “get their hands dirty” or learn the ins and outs of buying and operating properties. LPs in real estate syndications are often enticed by the great benefits that real estate ownership provides: cash flow, leverage, appreciation, and tax benefits.

Business partnerships, not real estate partnerships

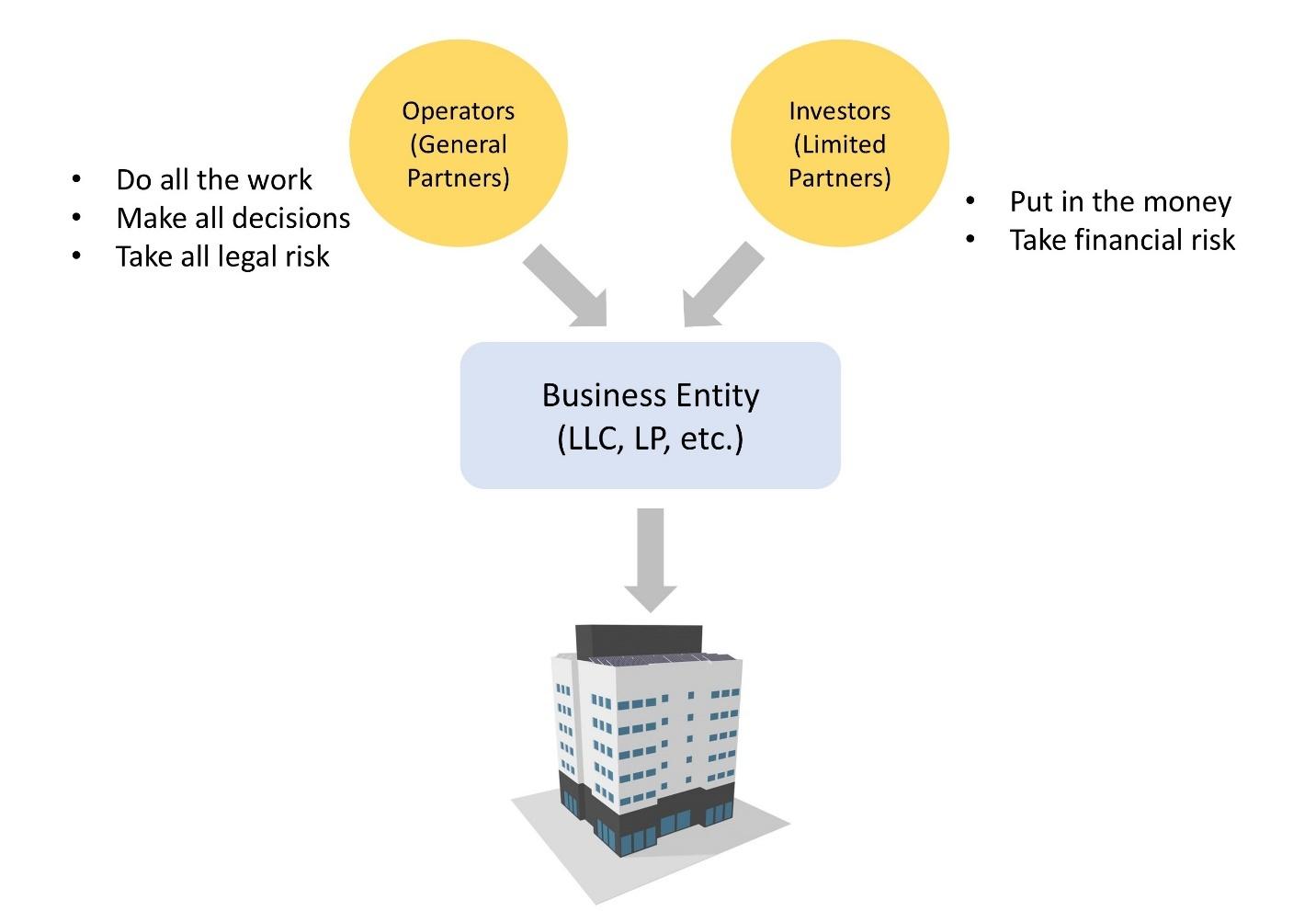

A syndication is structured as a business partnership. In fact, it may seem that GPs and LPs collectively invest directly in a piece of real estate, but that’s typically not the case.

The syndication is actually a business entity, often a limited liability company (LLC) or limited partnership (LP), where the GPs and LPs collectively hold ownership. In other words, when investing in a syndication as a passive investor (or being part of a syndication as an operator), your ownership is in a business entity, and that business entity is the owner of the real estate asset.

Long story short, a syndication is actually an investment into a business. And that business is the owner of the real estate or whatever other asset the syndication is choosing to purchase.

Let’s look at this visually:

Syndication Compliance

In legal parlance, a syndication is a “security,” which means passive investors are pooling their money with an operator who is responsible for generating returns on their behalf.

Anytime someone creates an investment offering where their efforts are being used to generate returns for other, nonactive and non-decision-making investors, that is a security. And in the United States, securities are governed by the Securities and Exchange Commission (SEC).

The SEC oversees securities transactions to protect investors. They require operators to follow specific rules and guidelines to ensure transparency and fairness when partnering with passive investors.

Registration requirements

Most securities must be registered with the SEC before being offered to the public. This registration process can take months or years, and can cost tens of thousands of dollars.

However, the SEC provides a faster path to offering securities through “exemptions,” which is simply a way for someone offering a security to do so without going through the formal registration process, so long as they adhere to certain conditions. The most common exemptions provided to real estate syndications by the SEC are under Regulation D, specifically Rule 506(b) and Rule 506(c) under that regulation:

- Rule 506(b): This exemption allows GPs to raise an unlimited amount of money from an unlimited number of accredited investors and up to 35 non-accredited investors, provided they meet certain sophistication requirements. Under this exemption, no public advertising of the security is allowed.

- Rule 506(c): This rule also allows for raising unlimited capital, but only from accredited investors. Unlike 506(b), 506(c) permits public advertising. And under this rule, the GP must take reasonable steps to verify that all investors in the security are accredited.

Accredited investor

You’ll notice that in the SEC exemptions most common to real estate syndications, there is a reference to accredited and non-accredited investors.

The SEC has decided that individual investors who meet a specific financial threshold should have more opportunity to invest in securities offerings based on their financial situation and presumed sophistication. They call this threshold accredited. To meet the definition of an accredited investor, an individual must meet one or both of the following criteria:

- Income test: The individual must have an annual income of at least $200,000 (or $300,000 combined with a spouse) for the last two years, and with the expectation of earning the same or more in the current year.

- Net worth test: The individual must have a net worth exceeding $1 million, either individually or jointly with a spouse, excluding the value of their primary residence.

In addition, individuals can meet the accredited threshold by holding certain broker licenses and professional credentials. And entities have their own separate rules to meet accredited status.

Syndication Documents

As mentioned, a syndication is a legal partnership. As such, there are legal documents that govern the partnership and the investment, so that both sides—the GPs and the LPs—know exactly what to expect from the business arrangement.

When investing in a syndication, there are five main documents that you should expect to receive to formalize the investment:

1. Private placement memorandum (PPM)

The PPM is a legal document provided by the GPs to potential investors, detailing the specific terms of the investment offering. It’s designed to provide investors with all the necessary information to make an informed decision about whether to invest in the syndication.

The PPM will typically include a summary of the investment, a list of risk factors associated with the investment, some legal disclosures, and—if not included elsewhere—the detailed financial projections you should expect from your investment.

The PPM is essentially a legal “insurance” for the GPs. It helps protect them by ensuring that all risks and terms are disclosed upfront, reducing the likelihood of disputes with investors down the line.

2. Subscription agreement

The subscription agreement is the legal contract between LP and the partnership. It outlines all the terms and conditions from the PPM, lays out your rights and obligations as an investor into the syndication and, upon signing, commits the LP to investing a specified amount of money into the syndication.

3. Partnership agreement

As mentioned, investing in a syndication is an investment in a business, not directly into a piece of property. As an investor, or shareholder, in a business, your rights and responsibilities as a shareholder are laid out in the partnership agreement or operating agreement that governs that business. This means that as part of your syndication commitment, you will be required to sign the partnership agreement or operating agreement.

4. Investor suitability form

It is the responsibility of the GPs to ensure that every LP investor into the syndication meets certain minimum requirements to invest. Not only must the GP team ensure that all LPs meet minimum compliance requirements (such as accreditation), but the GP will generally be on the hook to ensure that all LPs understand the risks associated with the investment and are in a financial position to sustain the potential loss of capital.

The investor suitability form allows the LPs to provide the financial information required for the GPs to make these determinations.

5. Business plan

In many cases, the GPs will prepare a presentation document (PDF, slide deck, etc.) that lays out the investment strategy and business plan for the particular investment. This presentation may include an overview of the GP team and their experience, information about the property and the location of the property, and details about the projection financial performance of the investment.

The business plan is often used to sell LPs on the investment, providing a compelling case for why the GPs believe the investment is a good one and why they are best suited to acquire and operate the investment.

How a Syndication Is Structured

The structure of a syndication deal can vary, but it generally includes a clear agreement on how profits will be shared, what fees will be paid to the GPs, and how the decision-making will take place.

Here’s a breakdown of the most common elements of a syndication structure:

Profit splits

The main reason to participate in a syndication is financial gain, so one key component of a syndication is how the profits are split between the GPs and LPs.

A typical syndication arrangement often has a profit split somewhere around 70/30. In other words, 70% of the profits would go to the LPs, while 30% of the profits would go to the GPs. This split will generally range from 60/40 to 90/10, depending on the specifics of the deal, but the most common is 70/30.

While this split of profits governs the overall division of profits, in practice, the specific agreement between the GPs and LPs is generally a bit more complicated, allowing each side some additional benefits to align interests in the investment. Specifically, the LPs often will have the additional benefit of a “preferred return,” while the GPs will have the additional benefit of collecting fees throughout the project.

Preferred return

A preferred return is a payment promised to the LPs prior to the GPs receiving their split of the profits. A common preferred structure provides for the LPs to receive a certain percentage of their investment (for example, 6%) in returns each year, before the GPs receive any part of the profit split.

For example, if an LP were to invest $100,000 in a syndication that offered a 6% preferred return, that investor would be entitled to $6,000 ($100,000 x 6%) each year of the investment before the GPs would be entitled to their portion of the profit split. This doesn’t mean $6,000 would be guaranteed to the LP in any given year (returns are never guaranteed in a syndication investment); if the syndication were unable to pay this investor $6,000 one year, the unpaid portion is added to the $6,000 owed the next year.

This balance will continue to accrue until the syndication is able to pay the owed amount, even if that accrued balance can’t be paid until the sale of the property. If for some reason the syndication never has enough profit to pay the LPs’ preferred returns, all available profit will go to the LPs, and the GPs will never be entitled to their share of the profits.

The use of a preferred return provides security to the LP that the GP will meet at least the minimum returns. If they can’t meet that minimum return hurdle, the GP will not get the benefit of the profits.

Note that preferred returns are common in syndications, but they are not universal. More recently, some syndications are choosing not to offer a preferred return to their LP investors.

Fees

We mentioned that LPs often have the benefit of a preferred return, ensuring that the passive investors receive a return before the operators receive any financial benefits. That isn’t completely true.

While GPs may not be entitled to a split of the profits before the preferred return is paid, syndication agreements often provide for the GPs to get paid fees throughout the transaction for managing the investment and hitting certain milestones. The fees will almost always take precedence over the preferred return and the profit split, nearly guaranteeing GPs some financial benefit from the project.

Common fees to GPs include:

- Acquisition fee: This is paid to the GPs for finding and purchasing the property and is often a percentage of the purchase price, typically between 1% and 3%.

- Asset management fee: An annual fee paid annually to the GPs for managing the asset. This is typically between 1% and 2% of the gross revenue the property generates.

- Capital transaction fee: This fee is similar to the acquisition fee, but is generated when a property is refinanced or sold. This is generally 1% of the refinance or sale amount.

- Construction management fees: If the property requires significant renovation, the GPs might earn a fee for managing the construction process, often between 5% and 7% of the total renovation costs spent.

These fees are designed to compensate the GPs for their time and expertise, as this is often the only compensation that a GP team will receive for the first year or two of ownership. While it’s important that GPs generate enough income to keep the business running, LPs should ensure that the fees being charged are reasonable and in line with those in the rest of the industry.

Hold period

The hold period is the length of time the property is expected to be owned before being sold. In many syndications, this period is between five and seven years, though it can vary based on the investment strategy. For example, a new construction development may be completed in 18 to 24 months, while the turnaround of an apartment complex may take five years or more.

During the hold period, the property is likely to undergo renovations and management improvement, all geared toward being able to increase income and profits, boosting the value of the property.

How Investors Make Money

LPs make money in a syndication in several different ways. And while financial expectations should be laid out as part of the business plan prior to an LP investing in a deal, financial performance is never guaranteed. It is important to understand how the operators expect the property to perform financially, but always expect deviations once the project starts.

Here are the five most common ways LPs benefit from a syndication:

1. Cash flow from operations

This is the income generated by the property after all expenses have been paid. It’s typically distributed to investors monthly or quarterly. As mentioned, LPs are often entitled to a preferred return prior to GPs receiving any portion of the cash flow. Once the preferred return is met, LPs and GPs split the cash flow based on the agreed-upon profit split.

Note that distributions to LPs from this cash flow may not be consistent. Depending on the condition of the property at purchase and other circumstances, there may not be much cash flow during the first couple of years of a project, and LPs may not receive much cash flow until the property is renovated and stabilized. Even then, cash flow will be dependent on actual operational performance, so some distributions may be larger than average, and some smaller.

2. Profits at sale

Real estate generally appreciates over time, and if the property’s value increases during the hold period, all members of the syndication will benefit when the property is sold. The appreciation can result from market forces, like rising property values, or from value-add strategies implemented by the GPs, such as renovations or improved management practices.

When the property is sold at the end of the hold period, the proceeds are first used to pay off any debt, then used to pay any owed preferred returns, and then finally, the remaining funds are split between the LPs and GPs based on the agreed-upon profit split. Proceeds from the sale often represent the largest payout for investors and are a key component of the syndication’s projected returns.

3. Tax benefits

Real estate investments come with significant tax advantages, including depreciation and interest deductions, which can be passed on to the LPs. Depreciation, in particular, can provide “paper losses” that offset other income, reducing the overall tax burden of the investors in the syndication.

Note that the ability to utilize tax benefits will be highly dependent on the personal situation of the investor. The promise of tax benefits from a syndication investment doesn’t mean that every LP will be able to use those benefits equally to offset other income or provide tax advantages. All LPs should consult with a tax professional to understand when and how they can benefit from syndication ownership.

Understanding Syndication Risks

While syndications offer attractive opportunities, they also come with risks that investors must understand. Here are four of them.

1. Market risk

The real estate market can be volatile, and changes in market conditions can impact property values and rental incomes. Economic downturns, rising interest rates, or changes in local market conditions can all negatively affect the performance of a syndication.

2. Operational risk

The success of a syndication largely depends on the ability of the GPs to execute on their business plan. Poor management, cost overruns, or delays in renovation projects can reduce the profitability of the investment. And there’s always the very real possibility that an investment results in a financial loss, which translates to investors losing some or all of their capital.

3. Liquidity risk

Real estate syndications are not liquid investments—once you invest, your capital is typically tied up for the duration of the hold period. If you need to access your money, it can be difficult or impossible to sell your share before the property is sold.

4. Financing risk

Most syndications involve the use of debt (leverage). Borrowing money to finance part of the purchase of the property can amplify gains when the project goes well, but it can also amplify losses when the project struggles. In other words, the use of debt adds significant risk to any syndication investment.

Final Thoughts

Real estate syndications provide an opportunity for two groups of people to join forces to make investments beyond the reach of either group alone. And when a syndication is structured correctly, both groups can leverage economies of scale to generate returns otherwise not available to either.