The private debt market of today has its roots in ancient forms of peer-to-peer lending in Mesopotamia, Egypt, Greece, and China, where loans were secured with crops and livestock, evolving into more structured financial systems over time.

In industrialized times of the last two centuries, private debt has found its modern form in response to economic and banking crises: the Great Depression in 1929, the savings and loan crisis of the 1980s, and of course, the Great Recession in 2008. It gained true momentum in the recent post-pandemic era.

In times of need, the local economy responds. I found this to be true in 2003; while I recognized the strong potential in real estate rental opportunities, my own capital constraints necessitated a more creative approach. A less conventional path ultimately connected me with a network of high-net worth individuals in Denver who were deploying capital through private lending. Their financing provided me with the liquidity needed to execute on opportunities that traditional lenders overlooked.

In hopes of helping real estate investors like me, I entered the real estate debt industry as a lender at the start of the Great Recession.

Private Credit in the 21st Century

In 2007, housing values had already started to drop. Interest rates were rising. Homeowners were defaulting. The years of easy access to money had come to an end—hastened by the collapse of Bear Stearns, Lehman Brothers, and more than 500 financial services institutions. The impacts were deep, widespread, and quick-moving, with devastation to the world economy.

In response to the crisis, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act in 2010. Dodd-Frank completely changed the lending paradigm, with 848 pages of financial reform. It established the Consumer Financial Protection Bureau (CFPB) to ensure fair lending practices, the Volcker Rule that restricted banks from speculative investments, stress-testing requirements for banks with “too big to fail” scenarios, and regulations that required greater transparency in derivatives market.

The result was reform, but it also led to a void. Banks were not only hesitant to lend but, in many cases, prohibited to do so.

Credit constraints only deepened further in the post-pandemic era, shifting from supply chain disruptions, excess stimulus, and labor market shifts to challenges of high inflation, rate hikes, and tightened liquidity.

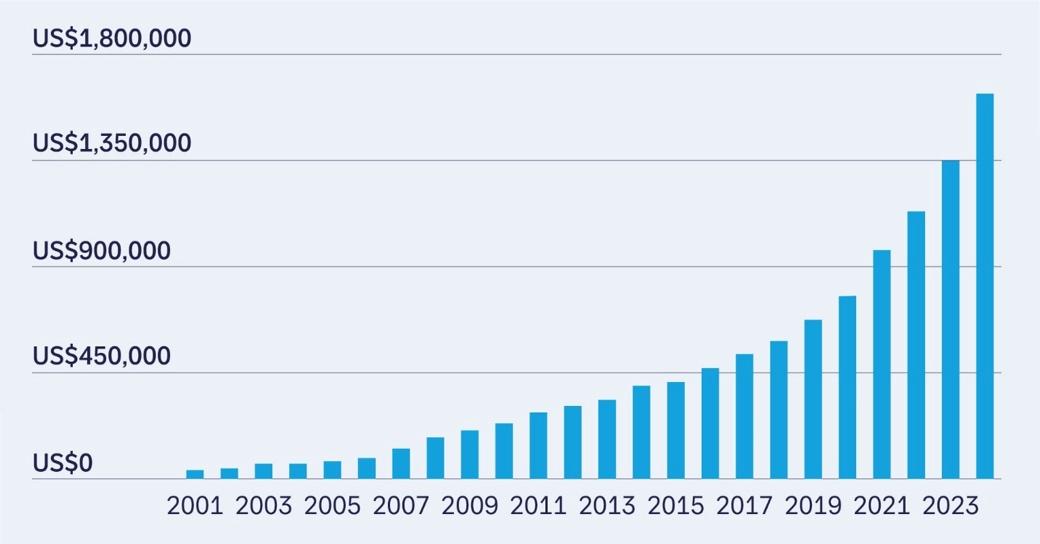

The numbers bear out this story. Private debt increased at 14% CAGR from $200 billion in 2007 to $1.8 trillion in 2024. (EY; flow by Deutsche Bank)

Figure 1 Flow from Deutsche Bank Corporate Bank article (2024)

The Gravity of Compliance

The new Trump administration will bring a softened regulatory climate, but banks are not likely or able to make a hard shift.

Since 2007, the banking sector has undergone significant consolidation— from 7,279 to 4,036 FDIC-commercial banks (FDIC). Four banks now control 44% of the nation’s banking assets (Financial Times). Eight Globally Systemically Important Banks (G-SIBs) are U.S.-based, but operate globally and under stringent international regulations within the Basel framework to standardize capital requirements, lending oversight, and liquidity management.

Even U.S. regional banks now have decades-long investments in compliance technology, talent, and culture that will not be easily reversed or abandoned. And a heavy reliance on traditional credit bureaus has limited the interpretation of credit for nontraditional borrowers in a post-pandemic economy, while failing to fully integrate real-time financial health and predictive analytics.

The banking sector’s risk posture is institutionalized. This has led to new partnerships and ecosystem models where traditional banks, like JPMorgan, Wells Fargo, and Citigroup, have joined forces with market players to participate in the booming private credit market—providing access with leverage lines, origination and credit platforms, and co-lending capabilities. Banks recognize that private credit lenders offer a fit-for-purpose business model and lower cost structure to achieve better yields. The market need for alternative solutions to restrictive lending, coupled with risks of ongoing inflation, higher rates, and policy uncertainty, shows no signs of abating.

In many cases, private credit lenders are the only option to sustaining current demand while keeping investor returns high.

The All-Weather Alternative

Market conditions have also amplified investor demand for stable rates of return and portfolio diversification. There is heightened exposure, correlation, and downside risk for investors utilizing traditional 60/40 portfolio allocations, or even those with a modest share of alternatives.

A shrinking number of public companies remain in the S&P 500, dominated by a handful of megacap technology firms. Years of consolidation, private equity buyouts, and companies opting to stay private longer have contributed to this shift— while high-value deals persist, overall M&A activity remains muted. Many firms are riding high in the AI boom; however, cracks in valuations are emerging due to competitive pressures from low-cost entrants like China’s DeepSeek and varying success rates of applied-use cases with a gap between hype and profitability.

Despite rallying bond prices late last year as inflation cooled, recent economic and policy uncertainty has kept the markets volatile with fluctuating yields. Rate cuts have led to corresponding reductions in high-yield savings, money market accounts, and expiring CDs—making those instruments less desirable.

In contrast, senior-secured direct lending has demonstrated resilient performance during economic ebbs and flows, offering downside protection through first-lien security. The lender has priority position in the capital stack in the event of a default and may carry lien insurance to guarantee the collateral. Specialty lenders also possess deep expertise in managing workouts to recapture intended value, with in-house and local networks proven in that asset class.

For example, in the real estate credit space, nimble business models, reasonable overhead, and expert risk structuring allow these specialty lenders to leverage fit-for-purpose loans with higher fees and collateral protection—enhancing profitability for the end-investor. These private lenders can transact with speed and certainty, which the market demands, and are deeply connected at the local economy level to react more precisely to regional dislocations.

This differentiated model also provides a contrast to larger, institutional private lenders, which operate at scale in larger deal sizes with greater exposure and, often, lack on-the-ground expertise with the asset.

When it comes to direct lending, resilience through economic downturns has been stress-tested, with Antares Capital reporting it as the only asset class to yield a gain in 2022.

Figure 2 Antares Capital Perspectives in Private and Liquid Credit (2025)

So, while uncertainty is an economic reality, regardless of the era, private credit remains a compelling diversification lever to strengthen portfolio probabilities.

The Growth Market Choice

According to BCG, private debt currently accounts for less than a quarter of global total assets under management, but generates more than half of investment-related wealth creation. BCG also projects that alternative assets will continue to deliver higher net revenue margin than traditional investments through at least 2028. (BCG Report 2024)

Michael Zawadzki, Blackstone Global CIO of Credit and Insurance, anticipates the market to grow to $25 trillion. (Bloomberg Interview)

There is no question that private debt is on a strong growth trajectory—driven by market demand and attractive returns for investors.

As always, investing requires diligence. Private credit lenders must operate with transparency, demonstrate a proven track record of capital preservation across economic cycles, and leverage specialized talent in a given asset class to expertly assess deal strength at the local level, and ensure the right returns from start to finish.

I have long believed in the first-mover advantage, and this market is no exception—even at its current dominant $1.8 trillion valuation. Investors today can capitalize on wider spreads and gather the unique intelligence and insights to act decisively before private credit transitions from mainstream adoption to ubiquity, where competition, commoditization, and regulation could reshape or dilute margins and yield.

About the Author

Kevin Amolsch formed Pine Financial Group, Inc in 2008 after leaving a small mortgage company as the senior loan officer for residential lending. Kevin started out in banking, working at First Bank in the lending department while in school. From there, he started his first real estate investment company, which is still active today.

He and his companies have closed on over 2,500 transactions as a buyer, seller, or private money lender. He is a two-time bestselling author, a sought-after expert in real estate finance and investing, and has been quoted in The Denver Post, The Denver Business Journal, The Las Vegas Review Journal, Forbes, Yahoo Real Estate, and many more.