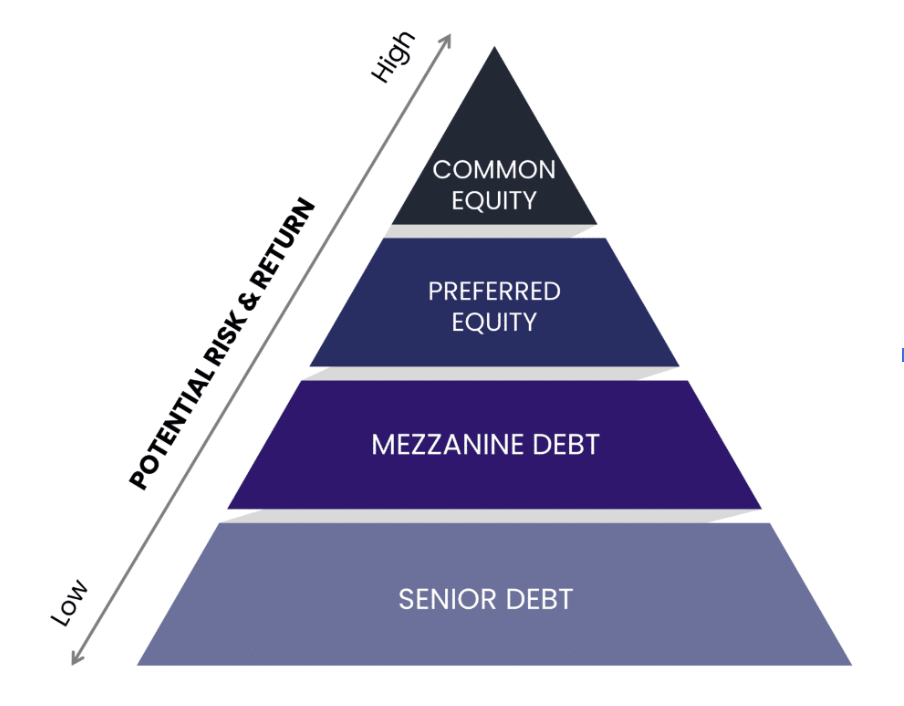

In the world of real estate investing, diversification is often associated with spreading investments across different markets, asset classes, and operators. But for passive investors, a truly resilient portfolio considers diversification within the capital stack itself—balancing equity and debt positions to achieve a mix of stability, growth, and adaptability to market shifts. This strategy not only provides a hedge against economic volatility, but also allows investors to take advantage of the specific benefits each layer offers.

Choosing the right mix between equity and debt is particularly relevant in today’s market, where credit availability fluctuates and economic cycles are unpredictable. Understanding how equity and debt work in the capital stack—and how to adjust your portfolio over time—can help you protect your wealth while maximizing opportunities.

Understanding Equity Investments in Real Estate

Equity investments in real estate provide investors with ownership stakes, meaning they benefit from both the property’s cash flow, possible appreciation, and potential tax benefits. While equity has higher potential returns, it also comes with higher risk, especially when market cycles enter periods of hypersupply or recession.

Advantages of equity investments

- Potential for high returns: Equity positions offer upside potential from appreciation and increased cash flows as properties gain value.

- Ownership and tax benefits: Equity holders often benefit from tax incentives like depreciation and capital gains treatment, enhancing their after-tax returns.

- An inflation hedge: Real estate assets tend to appreciate with inflation, protecting purchasing power.

Disadvantages of equity investments

- Higher risk: Equity sits higher in the capital stack, making it the last to receive returns if the property encounters financial challenges.

- Variable cash flow: Equity cash flows depend on property performance, which can be impacted by tenant turnover, operating costs (including repairs and maintenance), and market rents.

- Longer hold periods: Equity investments generally have longer hold periods and are more illiquid, especially during market downturns.

Equity investments are well suited for investors with a longer time horizon and higher risk tolerance. However, during certain phases of the market cycle—particularly in oversupplied or recessionary environments—equity investments can face greater volatility, emphasizing the importance of a balanced investment approach within the capital stack.

Understanding Debt Investments in Real Estate

Debt investments, typically structured as loans or mortgages, provide a more stable, lower-risk approach within the capital stack. Debt sits lower than equity, meaning debt investors are prioritized for returns before equity investors. For passive investors, debt can offer a potentially steady income with less volatility.

Advantages of debt investments

- Lower risk: Debt holders are the first to be repaid, reducing exposure to property performance risks.

- Steady cash flow: Debt investments often provide fixed income through interest payments, appealing to investors who prioritize stability.

- Compounding potential: Some debt funds allow investors to reinvest returns, effectively compounding their growth. For instance, if an investor places $100,000 in a debt fund offering an 8% preferred return and chooses to compound rather than take monthly cash flow, the investment could grow to a 17.1% annualized return over 10 years.

Disadvantages of debt investments

- Limited upside: Debt investors earn fixed returns and don’t benefit from property appreciation, capping the potential gain.

- Fewer tax benefits: Unlike equity, debt investments generally don’t offer tax benefits like depreciation.

Debt investments appeal to investors who prioritize capital preservation and steady cash flow. While debt might offer more stability in turbulent markets, it may underperform equity investments during expansion phases when property values rise rapidly.

Equity vs. Debt: Key Factors to Consider

To choose the right balance between equity and debt, passive investors should evaluate these factors:

- Time horizon: Investors with longer-term perspectives may benefit more from equity investments that appreciate over time. Debt is better suited for shorter-term goals or for generating steady cash flow.

- Risk tolerance: Equity carries more volatility, but offers higher returns. Debt provides more security, especially during market downturns, as it’s lower in the capital stack.

- Financial goals: Your choice should align with whether you’re in an accumulation phase (focused on growing wealth) or a cash flow phase (focused on generating income). Also, you should lay a plan for your needs five to 10 years out as well.

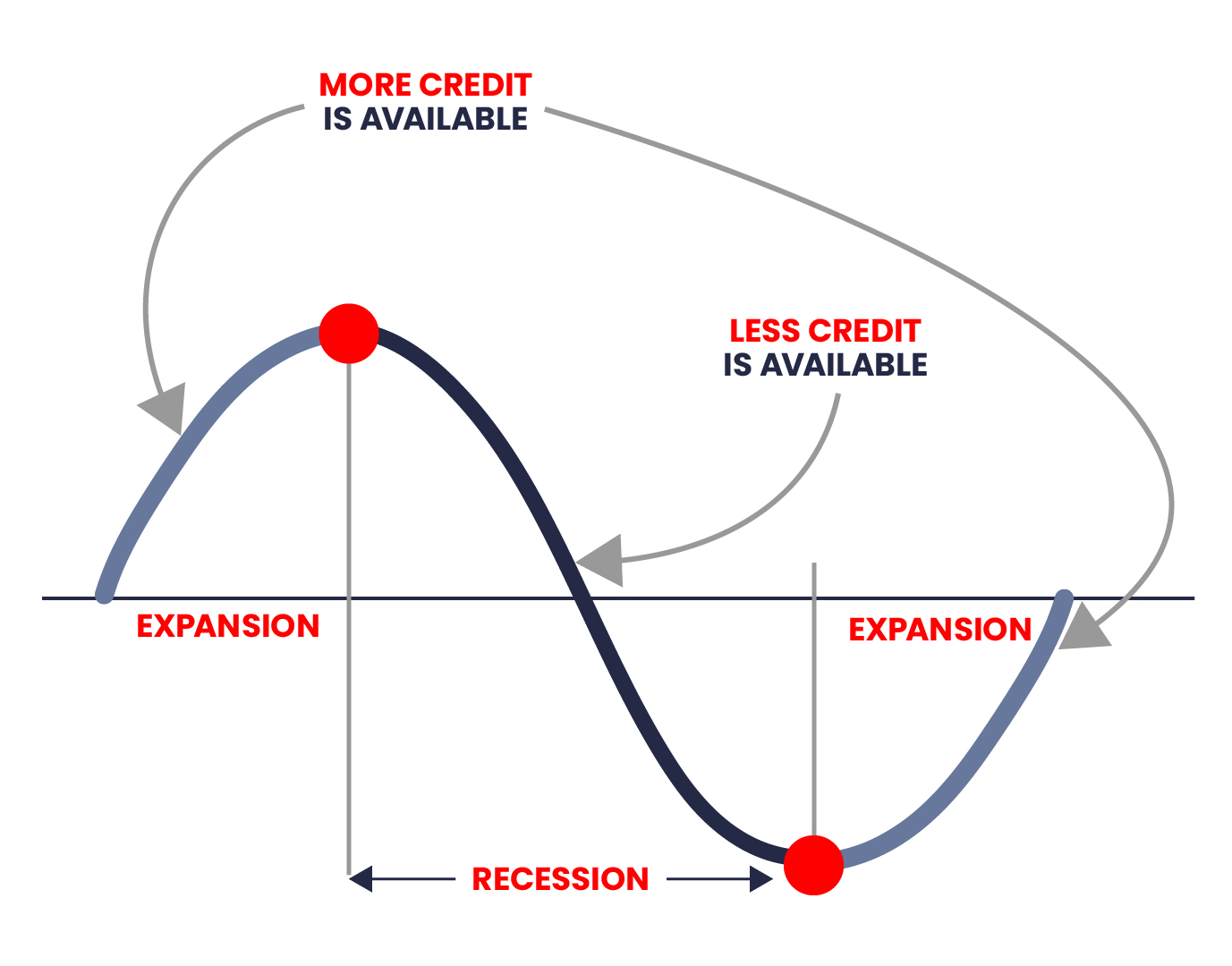

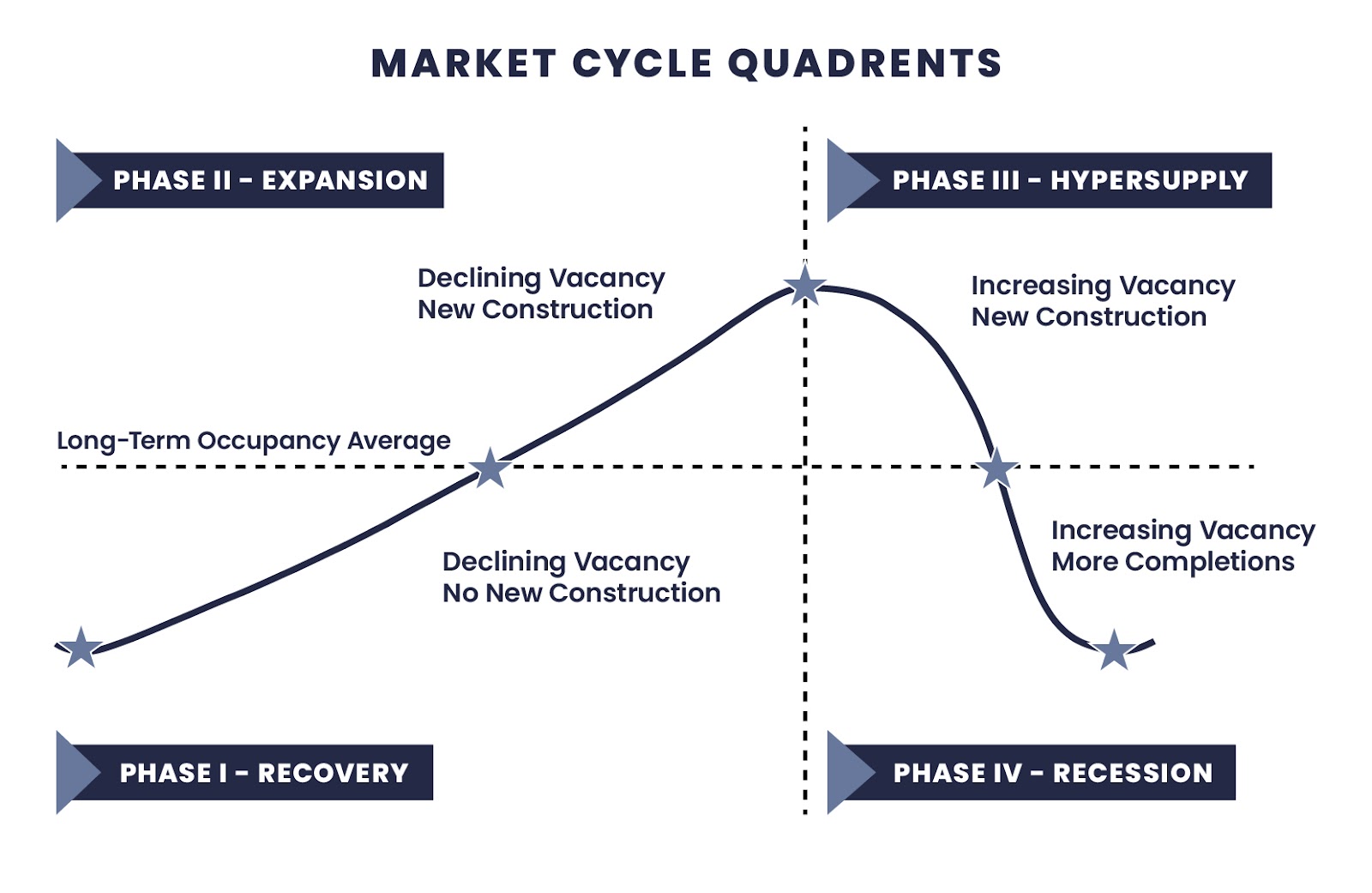

- Market and debt cycles: Another critical factor is the market cycle and credit availability. Equity investments can be riskier during a hypersupply phase or when credit is scarce, as refinancing options become limited. Debt investments, on the other hand, tend to offer stability in downturns, but may yield lower returns during expansions. (Refer to the market cycle charts to visualize these phases.)

Debt cycle

Market cycle

Portfolio Tracking: The Key to an Informed, Balanced Investment Approach

Once you establish a diversified capital stack, the next step is ongoing portfolio tracking. Passive investors should be able to assess their portfolio at any point, knowing how much is invested in each deal, operator, market, asset class, and capital stack position. This level of insight helps prevent overexposure in any one area and reveals under-allocated opportunities for growth.

While building a tracking system may seem tedious, it’s a fundamental skill that can save—and even make—significant amounts over time. Consistent tracking not only shows where adjustments may be needed, but also provides an accurate picture of how well the current portfolio aligns with market conditions and personal financial goals.

Case Studies: Applying Capital Stack Diversification to Different Investor Profiles

To make this strategy more actionable, let’s consider three example investor profiles and how they might approach equity and debt allocation within the capital stack.

1. Late-stage accumulator

Scenario: This investor, aged 55, has 10 years until retirement and wants to build wealth quickly without taking excessive risks.

Strategy:

- They invest $250,000 in equity positions within a stabilized multifamily property for growth potential. Assuming a 12% annualized return, this portion could grow to over $775,000 in 10 years if market conditions hold steady.

- To balance this, they also place $150,000 in a real estate debt fund offering an 8% preferred return with compounding. By reinvesting the distributions, this portion would grow to roughly $323,000 over the same period, adding a layer of stability to the overall portfolio.

By combining equity for growth and compounding debt for security, this investor positions themselves to accumulate wealth with a balance of risk and cash flow.

2. Retiree with an established portfolio

Scenario: This investor, aged 70, has a substantial net worth and prioritizes stability and income preservation.

Strategy:

- They allocate $500,000 to debt investments for steady cash flow, with an expected 8% return. This allocation provides $40,000 annually in passive income, supporting their lifestyle without drawing down principal.

- They reserve a smaller portion—$100,000—for selective equity investments in inflation-resistant assets, like commercial properties with long-term leases. This balance allows them to hedge against inflation without significantly increasing risk.

For this retiree, prioritizing debt in the capital stack aligns with their need for stability, while a smaller equity position offers protection against inflation.

3. Younger investor with time

Scenario: This investor, aged 35, is in the accumulation phase with a high-risk tolerance and a 20-year-plus investment horizon.

Strategy:

- They place $200,000 in equity investments across multiple markets, expecting a 12% annualized return. If this growth rate holds, their equity could grow to over $1.3 million in 20 years.

- For balance, they invest $50,000 in a compounding debt fund with an 8% preferred return. This fund grows to about $233,000 over the same period, adding a stable component to their high-growth portfolio.

This mix allows the younger investor to maximize growth through equity while having a safety net in debt, supporting long-term wealth accumulation.

Conclusion: Finding the Right Balance in the Capital Stack

Determining the right mix of equity and debt within the capital stack is a strategic decision that should evolve with your financial goals, risk tolerance, and market conditions. By diversifying across the capital stack and regularly reassessing your portfolio, you create a framework for long-term resilience that can withstand both expansionary and recessionary periods.

For passive investors, tracking exposure across deals, operators, markets, asset classes, and the capital stack itself is crucial. With this informed approach, you can seize opportunities and mitigate risks in a way that aligns with your unique investment journey.

About Whitney Elkins-Hutten

Whitney Elkins-Hutten is the Director of Investor Education at PassiveInvesting.com, Founder of AshWealth.com, author of Money for Tomorrow: How to Build and Protect Generational Wealth published with BiggerPockets, co-author of the international #1 bestseller Resilient Women in Life and Business, host of the Passive Investing Made Simple YouTube show and podcasts, and a partner in $800MM+ in real estate — including over 6500+ residential units, 15 express car washes, and more than 2200+ self-storage units across 11 states—and experience flipping over $5MM in residential real estate.

Whitney’s Social Handles

- PassiveInvestingWithWhitney.com

- Author of Money for Tomorrow: How to Build and Protect Generational Wealth published with BiggerPockets